The Ultimate Guide to Benefits in Kind: 2025 Complete UK Tax and Compliance Guide

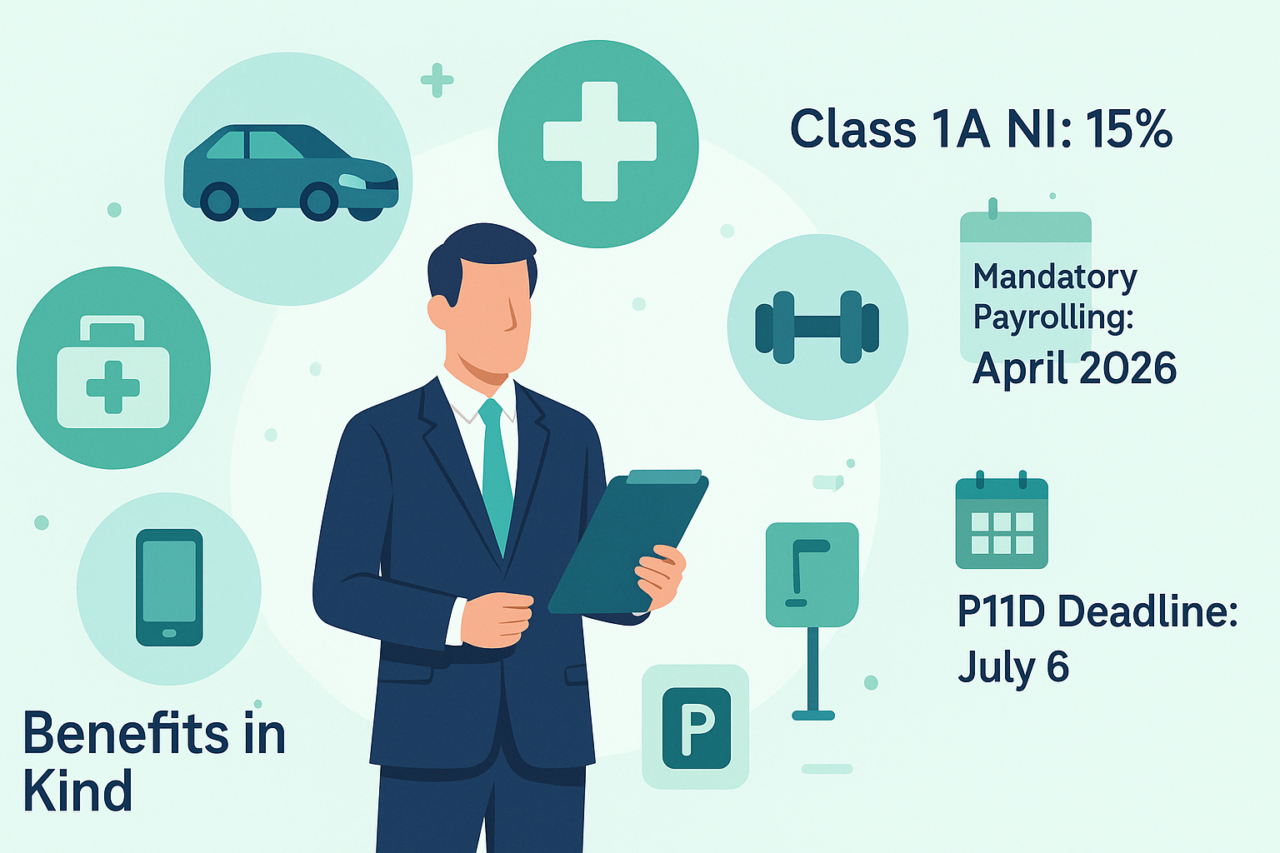

Benefits in kind (BIKs) are non-cash perks provided by employers to employees that have monetary value and are subject to taxation. With mandatory payrolling of benefits starting April 2026 and Class 1A National Insurance rates increasing to 15% from April 2025, understanding BIK taxation has become crucial for UK employers and employees. Common examples include company cars (with electric vehicles at favorable 2% BIK rates until 2025/26), private medical insurance, gym memberships, and mobile phones, with tax treatment varying significantly based on benefit type and usage patterns.

What is a Benefit-in-Kind (BIK)? Complete Definition and Framework

A benefit-in-kind (BIK) is any non-cash benefit of monetary value that an employer provides to an employee for their personal use, beyond what is wholly, exclusively, and necessary for business purposes. These "fringe benefits" supplement an employee's salary and are subject to taxation because they effectively increase an employee's overall income.

Key Characteristics of Benefits in Kind:

- Non-cash nature: Not provided as direct monetary payment

- Personal benefit: Available for employee's private use

- Monetary value: Can be assigned a cash equivalent value

- Tax implications: Subject to income tax and potentially National Insurance contributions

- Employment-related: Provided by virtue of the employment relationship

Legal Framework and HMRC Definition:

HMRC considers BIKs as earnings from employment under Income Tax (Earnings and Pensions) Act 2003. The taxation principle ensures employers cannot substitute salary with benefits to avoid tax obligations, maintaining fairness across different compensation structures.

Current Benefits in Kind Tax Rates and National Insurance: 2025 Update

Class 1A National Insurance Rates:

- 2024/25 rate: 13.8%

- 2025/26 rate: 15% (increased from April 6, 2025)

- Payable by: Employers only (employees don't pay NI on BIKs)

- Payment deadline: July 19 (cheque) or July 22 (online) following tax year end

Income Tax Treatment:

BIKs are added to employee's taxable income and taxed at their marginal rate:

- Basic rate (20%): Income up to £50,270

- Higher rate (40%): Income £50,270 - £125,140

- Additional rate (45%): Income above £125,140

Calculation Example:

Company car BIK value: £5,000 annually

- Employee tax (40% bracket): £2,000

- Employer Class 1A NI (15%): £750

- Total tax cost: £2,750

Common Examples of Benefits in Kind: Comprehensive Analysis

1. Company Cars: Most Complex BIK Category

Tax Calculation Factors:

- P11D value: List price including VAT and optional extras

- CO2 emissions: Determines percentage band for tax calculation

- Fuel type: Electric, hybrid, petrol, or diesel classifications

- Employee's tax bracket: 20%, 40%, or 45%

2025/26 BIK Rates by Vehicle Type:

- Electric vehicles: 2% (increasing to 3% in 2025/26, then 1% annually)

- Ultra-low emission (<75g/km CO2): Starting from 14%

- Petrol/diesel vehicles: 25-37% depending on emissions

- Diesel supplement: Additional 4% (maximum 37%) unless RDE2 compliant

Favorable Electric Vehicle Treatment: Government incentives make electric company cars highly tax-efficient, with BIK rates remaining under 10% until 2030, compared to 25%+ for conventional vehicles.

2. Private Medical Insurance: Popular Employee Benefit

Tax Treatment:

- Taxable amount: Full premium cost paid by employer

- Employee tax: Based on marginal tax rate (20%, 40%, or 45%)

- Employer Class 1A NI: 15% on premium value

- Reporting: Via P11D or payroll system

Typical Costs and Tax Impact:

- Premium cost: £1,200 annually

- Employee tax (40% bracket): £480

- Employer NI: £180

- Total tax cost: £660

3. Gym Memberships and Wellness Benefits

Tax Threshold:

- Exempt amount: £15.60 per week per employee

- Taxable excess: Amount above threshold subject to full BIK treatment

- Reporting requirement: Must be reported if exceeding exempt amount

4. Mobile Phones: Commonly Exempt Benefit

Tax-Free Provision:

- One phone per employee: Completely exempt from tax and NI

- Business and private use: No apportionment required

- Line rental and calls: Employer-paid charges are tax-free

- Multiple phones: Second and subsequent phones are taxable BIKs

5. Company Vans: Alternative to Car Provision

2025/26 Tax Rates:

- Van benefit charge: £4,020 annually

- Van fuel benefit: £769 annually (if private fuel provided)

- Double cab pickups: From April 2025, most treated as cars rather than vans

- Significant private use: Full charge applies unless purely business use

6. Interest-Free and Low-Interest Loans

Tax Treatment:

- £10,000 threshold: Loans below this amount are exempt

- Official interest rate: Currently variable, reviewed quarterly from April 2025

- Taxable benefit: Difference between official rate and actual rate charged

- Loan forgiveness: Written-off amounts are fully taxable

7. Accommodation Benefits: Complex Calculations

Basic Annual Value:

- Calculation basis: Higher of annual letting value or rent paid by employer

- Employee contributions: Deductible from taxable value

- Expensive accommodation: Additional charges apply if cost exceeds £75,000

Additional Charges:

- Council tax/utilities: Usually treated as separate taxable benefits

- Furniture and services: May create additional BIK liabilities

8. Childcare and Family Benefits

Childcare Vouchers:

- Existing schemes: Grandfathered arrangements continue with tax advantages

- New entrants: Tax-Free Childcare replaced vouchers for new participants

- Salary sacrifice: Available through existing schemes only

Tax-Exempt Benefits: Complete List of Non-Taxable Perks

Workplace-Related Exemptions:

- Workplace parking: Free parking at or near workplace

- Workplace nurseries: On-site childcare facilities

- Staff restaurants: Subsidized meals available to all employees

- Work buses: Transport services for multiple employees

Health and Safety Exemptions:

- Eye tests and glasses: For VDU users only

- Medical check-ups: Health screenings and occupational health

- Workplace first aid: Basic medical facilities and treatment

Training and Development:

- Work-related training: Skills development directly related to employment

- Retraining courses: Career development and skill enhancement

- Professional subscriptions: Relevant professional body memberships

Minor Benefits:

- Trivial benefits: Under £50 per occasion, maximum £300 annually for directors

- Long service awards: After 20+ years service, up to £50 per year of service

- Staff suggestion schemes: Awards for implemented suggestions

Cycle-to-Work Scheme:

- Complete exemption: Bicycles and safety equipment provided for commuting

- Salary sacrifice: Tax and NI savings for both employer and employee

- Transfer conditions: Specific rules for ownership transfer after scheme period

Key Differences: Benefits in Kind vs. Salary Sacrifice

Benefits in Kind:

- Additional to salary: BIKs supplement existing salary arrangements

- Tax treatment: Subject to income tax at marginal rates

- NI treatment: Employers pay Class 1A NI at 15%

- Employee choice: Employer determines benefit provision

- Flexibility: Can be withdrawn or modified by employer

Salary Sacrifice:

- Salary reduction: Employee agrees to reduce gross salary

- Tax advantages: Potential savings on both income tax and National Insurance

- Employee consent: Requires explicit agreement and documentation

- Limited benefits: Only certain benefits qualify for salary sacrifice treatment

- Contractual: Creates binding obligation between employer and employee

Qualifying Salary Sacrifice Benefits:

- Pension contributions

- Cycle-to-work schemes

- Ultra-low emission vehicles

- Childcare vouchers (existing arrangements only)

Purpose and Strategic Value of Offering Benefits in Kind

Talent Acquisition and Retention:

- Market differentiation: BIKs help employers stand out in competitive markets

- Total compensation: Enhances overall package value beyond basic salary

- Employee preferences: 57% of employees want health and wellness benefits from employers

- Retention impact: Comprehensive benefits reduce turnover by 25-30%

Employee Wellbeing and Productivity:

- Health support: Medical insurance and wellness programs improve employee health

- Work-life balance: Flexible benefits help employees manage personal responsibilities

- Financial assistance: BIKs like company cars reduce employee expenses

- Stress reduction: Comprehensive benefits decrease financial and health-related stress

Tax Efficiency Opportunities:

- Employer deductions: Most BIK costs are allowable business expenses

- Employee tax planning: Some benefits taxed more favorably than equivalent salary

- National Insurance savings: Certain arrangements reduce overall NI liability

- Salary sacrifice synergies: Integration with salary sacrifice for optimal tax efficiency

Mandatory Payrolling: April 2026 Changes and Preparation

Current Reporting Options (Until April 2026):

- P11D Forms: Annual reporting by July 6 following tax year end

- Voluntary Payrolling: Real-time reporting through payroll systems (requires pre-registration)

Mandatory Changes from April 2026:

- Universal payrolling: All employers must payroll most BIKs

- P11D elimination: Forms P11D will be phased out for most benefits

- Class 1A NI payrolling: National Insurance also processed through payroll

- Real-time reporting: Monthly or weekly reporting depending on payroll frequency

Exceptions Remaining After 2026:

- Beneficial loans: Will remain on voluntary payrolling initially

- Living accommodation: P11D reporting continues temporarily

- Complex benefits: Some arrangements may retain annual reporting

Preparation Requirements:

- Payroll software upgrade: Must be HMRC-approved and capable of BIK processing

- System integration: Benefits administration must connect with payroll systems

- Process redesign: Monthly benefit valuation instead of annual calculations

- Staff training: Payroll and HR teams need upskilling for new requirements

Implementation Timeline:

- June-December 2025: HMRC publishes detailed technical specifications

- January-March 2026: Final system testing and staff training

- April 6, 2026: Mandatory payrolling begins

How to Report Benefits in Kind: Current and Future Methods

Current P11D Reporting Process:

- Form P11D: Complete for each employee receiving taxable benefits

- Form P11D(b): Summary return calculating total Class 1A NI liability

- Deadline: July 6 following end of tax year

- Employee copies: Provide P11D copies to employees by July 6

- NI payment: Pay Class 1A National Insurance by July 19/22

Voluntary Payrolling (Available Now):

Registration Requirements:

- Register with HMRC before start of tax year

- Specify which benefits will be payrolled

- Ensure payroll software compatibility

- Obtain employee consent where required

Operational Process:

- Calculate benefit values monthly/weekly

- Add to gross pay for tax purposes (no cash paid)

- Deduct income tax through PAYE

- Still complete P11D(b) for Class 1A NI

- Report through RTI submissions

Benefits of Early Payrolling Adoption:

- Cash flow: Spread tax payments throughout year rather than lump sum

- Employee clarity: Tax deducted regularly, no year-end surprise bills

- Administrative efficiency: Reduced year-end compliance burden

- Future preparation: Experience with systems before mandatory introduction

Designing Effective Benefits in Kind Packages: Strategic Framework

Employee Needs Assessment:

Demographics Analysis:

- Age groups: Different generations prioritize different benefits

- Family status: Single vs. family-oriented benefit preferences

- Income levels: Tax efficiency varies by marginal tax rates

- Commuting patterns: Transport-related benefits relevance

Survey and Feedback Methods:

- Annual benefits surveys and preference questionnaires

- Focus groups for detailed benefit discussions

- Exit interview analysis of departing employees

- Benchmarking against industry and local competitors

Budget Planning and Cost Analysis:

Total Cost Calculation:

- Benefit provision costs (premiums, purchase prices)

- Class 1A National Insurance at 15%

- Administrative and compliance costs

- Payroll system upgrades and maintenance

ROI Measurement:

- Employee retention cost savings

- Recruitment advantage and faster hiring

- Productivity improvements from healthier, happier employees

- Tax efficiency gains from strategic benefit selection

Benefit Mix Optimization:

High-Impact, Low-Cost Options:

- Workplace parking (completely tax-free)

- Cycle-to-work schemes (tax-free and popular)

- Trivial benefits (£50 per occasion limit)

- Mobile phones (one per employee tax-free)

Premium Benefits for Key Staff:

- Company cars (especially electric vehicles)

- Private medical insurance

- Enhanced pension contributions

- Professional development opportunities

Flexible Approaches:

- Cafeteria-style benefit selection

- Different tiers for different employee levels

- Seasonal or temporary benefit offerings

- Integration with salary sacrifice options

Tax Planning Strategies for Benefits in Kind

Employer Tax Efficiency:

Allowable Deductions:

- All BIK provision costs are generally deductible business expenses

- Class 1A National Insurance is deductible against corporation tax

- Professional advice and administration costs are allowable

- Payroll system upgrades may qualify for capital allowances

Timing Strategies:

- Accelerate benefit provision in high-profit years

- Defer expensive benefits to manage cash flow

- Coordinate with salary sacrifice schemes for maximum efficiency

- Plan around accounting year ends for optimal tax treatment

Employee Tax Planning:

Benefit Selection Optimization:

- Consider marginal tax rates when choosing benefits

- Evaluate total tax cost (income tax + employer NI)

- Compare BIK taxation with cash equivalent

- Utilize tax-free benefits wherever possible

Timing Considerations:

- Spread benefit utilization across tax years where possible

- Consider impact on other tax calculations (student loans, child benefit)

- Plan major benefits around income fluctuations

- Coordinate with salary sacrifice arrangements

Common Compliance Pitfalls and How to Avoid Them

Record-Keeping Failures:

Essential Documentation:

- Benefit provision agreements and employee consents

- Purchase invoices, receipts, and contract documentation

- Usage logs for shared benefits (company cars, phones)

- Valuation calculations and supporting evidence

Digital Record Systems:

- Cloud-based storage for accessibility and backup

- Integration with payroll and HR systems

- Audit trails for all benefit-related transactions

- Regular data backups and disaster recovery plans

Valuation Errors:

Common Mistakes:

- Using net costs instead of gross amounts including VAT

- Failing to include all optional extras and accessories

- Incorrect apportionment between business and private use

- Outdated official rates and thresholds

Accurate Valuation Process:

- Regular updates of official rates and thresholds

- Professional valuation for complex benefits

- Cross-checking calculations with HMRC guidance

- Annual review of all benefit valuations

Deadline Management:

Critical Dates Calendar:

- April 5: Last day for payrolling registration for following tax year

- July 6: P11D and P11D(b) submission deadline

- July 19/22: Class 1A National Insurance payment deadline

- Ongoing: Monthly/weekly payrolling submissions under mandatory system

Employee Communication:

Clear Information Provision:

- Annual benefit statements showing cash values and tax implications

- Regular updates on benefit changes and tax rates

- Educational materials on tax-efficient benefit utilization

- Access to professional advice for complex situations

Future Trends and Developments in Benefits in Kind

Technology Integration:

- AI-powered benefit selection: Personalized recommendations based on employee profiles

- Blockchain verification: Immutable records for compliance and audit trails

- Mobile-first administration: Employee self-service through smartphone apps

- Predictive analytics: Anticipating benefit needs and utilization patterns

Regulatory Evolution:

- Digital-first compliance: Full integration with Making Tax Digital requirements

- Real-time reporting: Expansion beyond current RTI to include all benefit types

- International alignment: Coordination with global mobility and cross-border employment

- Environmental incentives: Enhanced tax treatment for sustainable and green benefits

Benefit Innovation:

- Sustainability focus: Carbon offset programs and environmental benefits

- Mental health expansion: Comprehensive psychological wellbeing support programs

- Financial wellness: Debt counseling, savings programs, and financial education

- Flexible working support: Enhanced technology and home office provision

Market Predictions 2025-2027:

- Electric vehicle dominance: BIK advantages driving EV adoption in company fleets

- Health benefit expansion: Post-pandemic focus on comprehensive medical support

- Personalization growth: Individual benefit selection replacing standard packages

- Compliance automation: AI and machine learning reducing administrative burden

Key Takeaways: Mastering Benefits in Kind

Strategic Importance: Benefits in kind have evolved from simple perks to strategic tools for talent attraction, retention, and employee wellbeing. Understanding their tax implications and compliance requirements is essential for effective implementation and avoiding costly mistakes.

Tax Planning Imperative: With Class 1A National Insurance increasing to 15% from April 2025 and mandatory payrolling beginning April 2026, employers must review benefit strategies, upgrade systems, and train staff to manage new compliance requirements effectively.

Employee Value Creation: Well-designed BIK packages can provide significant value to employees while managing tax efficiency. Focus on tax-free benefits where possible, consider employee demographics and preferences, and integrate with salary sacrifice schemes for optimal results.

Compliance Excellence: Accurate record-keeping, timely reporting, and professional advice are essential for BIK compliance. Prepare now for mandatory payrolling by upgrading systems, training staff, and establishing robust benefit valuation processes.

Future-Proofing Strategy: The BIK landscape continues evolving with technology integration, regulatory changes, and shifting employee expectations. Successful employers will adapt their benefit strategies while maintaining compliance and maximizing value for both business and employees.

The ultimate success in benefits in kind lies in balancing employee value, tax efficiency, and compliance requirements while adapting to ongoing regulatory and technological changes in the UK employment landscape.

Frequently Asked Questions: Benefits in Kind

What benefits in kind are completely tax-free in 2025?

Tax-free benefits include workplace parking, one mobile phone per employee, cycle-to-work schemes, trivial benefits under £50 per occasion, workplace nurseries, staff restaurants available to all employees, work-related training, and eye tests for VDU users. These exemptions help employers provide valuable perks without tax implications.

How will mandatory payrolling from April 2026 affect my business?

From April 2026, you must process most benefits through payroll monthly rather than annual P11D forms. This requires HMRC-approved payroll software, monthly benefit valuations, and real-time tax deductions. While initially complex, it provides better cash flow management and eliminates year-end compliance burdens.

What's the difference between P11D reporting and payrolling benefits?

P11D reporting involves annual forms submitted by July 6, with employees paying tax through code adjustments or self-assessment. Payrolling involves monthly tax deductions through regular payroll, providing immediate tax collection and better employee clarity about benefit costs.

How are company car benefits calculated for tax purposes?

Company car BIK is calculated by multiplying the car's P11D value (list price including VAT and extras) by the appropriate percentage band based on CO2 emissions, then multiplying by the employee's marginal tax rate. Electric vehicles benefit from favorable 2% rates in 2024/25, increasing gradually to 5% by 2027/28.

Can employees pay for part of a benefit to reduce the tax charge?

Yes, employees can make good part or all of a benefit's cost to reduce the taxable amount. Payments must be made by July 6 following the tax year end. However, for some benefits like company cars, partial payments don't reduce the BIK percentage - only affect fuel benefits.

What happens if I don't report benefits in kind correctly?

Incorrect reporting can result in penalties, interest charges, and back-dated tax assessments. HMRC can investigate up to 6 years of historical BIK arrangements. Penalties range from careless errors (20% of tax due) to deliberate concealment (100% of tax due), making accurate reporting essential.

How does the Class 1A National Insurance increase to 15% affect benefit costs?

The increase from 13.8% to 15% in April 2025 adds £120 annual cost per £10,000 of BIK value. For employers providing significant benefits like company cars or medical insurance, this represents substantial additional costs requiring budget adjustments and possible benefit strategy reviews.